If you have ever walked into a Japanese bank armed with your residence card and a confident attitude, only to be handed a form asking for your inkan, you will know the particular deflation of that moment. A hanko—specifically, a bank account Japan hanko—is one of those requirements that catches foreigners off guard precisely because it seems anachronistic. You have a passport, a residence card, a phone, a face. Surely that is enough. At many Japanese banks, it is not.

The situation has evolved in recent years. Some banks have moved toward accepting signatures from foreign customers, and a handful of digital-first institutions have removed the seal requirement entirely. But at the majority of traditional Japanese banks—the ones where salary gets deposited, where utility direct debits are set up, where a landlord might insist you bank—a hanko is still expected or at least strongly preferred.

This guide explains why banks ask for seals, when a signature might be accepted instead, what kind of hanko to use for banking purposes, and what to bring when you walk in. Whether you are opening your first account after arriving in Japan or finally sorting out a proper bank after relying on convenience store ATMs for too long, this is the practical side of Japan banking for foreigners that most orientation packets leave out.

Why banks ask for seals

The hanko’s role in Japanese banking is not bureaucratic stubbornness. It has a functional logic rooted in how Japanese financial institutions have historically verified identity and authorised transactions.

A seal registered with a bank—called a ginkoin (銀行印)—creates a second layer of verification beyond the passbook or cash card. When you submit a withdrawal slip or certain account instructions in person, the bank compares the impression on the form against the impression on file. If they match, the transaction proceeds. If they do not, it stops. In an era before widespread biometric verification and two-factor authentication, this was a reliable, low-tech fraud deterrent.

The system persisted because it worked and because changing it requires updating decades of internal procedure across thousands of branches. Japan’s banking sector is notably conservative about operational change, and while digital verification is gradually making inroads, the seal remains embedded in branch-level processes at most major institutions.

For foreign customers, the bank seal requirement has an additional layer of complexity: your name in romaji does not naturally fit the same stamp format as a Japanese name in kanji. This has led to varying policies across institutions, with some banks accepting katakana hanko, some accepting romaji, and some accepting a signature in lieu of a seal for foreign account holders specifically.

Once you land a job via ComfysCareer, you will need a bank account for salary—this guide helps you prepare the hanko side.

When a signature may be accepted

The short answer: at some banks, for some account types, under certain conditions.

Japan Post Bank (ゆうちょ銀行) and several regional banks have quietly expanded signature acceptance for foreign nationals in recent years. Some branches of major banks like MUFG, SMBC, and Mizuho will allow a signature instead of a seal for foreign customers, particularly at branches in areas with large international populations. The key word is “branch”—policy implementation is not always uniform, and what one branch accepts, another may not.

Digital banks and fintech-adjacent institutions have moved furthest from the seal requirement. Rakuten Bank, PayPay Bank, and Sony Bank operate largely or entirely online and do not require a physical hanko for account opening. For foreigners who primarily need a functioning account for salary deposits, online shopping, and bill payment, these can be a practical choice.

Consider two scenarios. Hiroshi, a Brazilian-Japanese dual national living in Nagoya, opened a Mizuho account at a branch near his workplace. The staff accepted his signature after a brief internal consultation, noting his foreign nationality on the account record. Meanwhile, Sophie, a French teacher in a smaller city in Shikoku, was firmly told a hanko was required at the local branch of the same bank. Same institution, different outcomes. If a signature is important to you, calling ahead to ask specifically is always worth thirty seconds.

That said, even where signatures are accepted today, having a ginkoin on hand signals preparation and reduces friction in every subsequent bank interaction. Japanese banking staff respond well to customers who have done their homework.

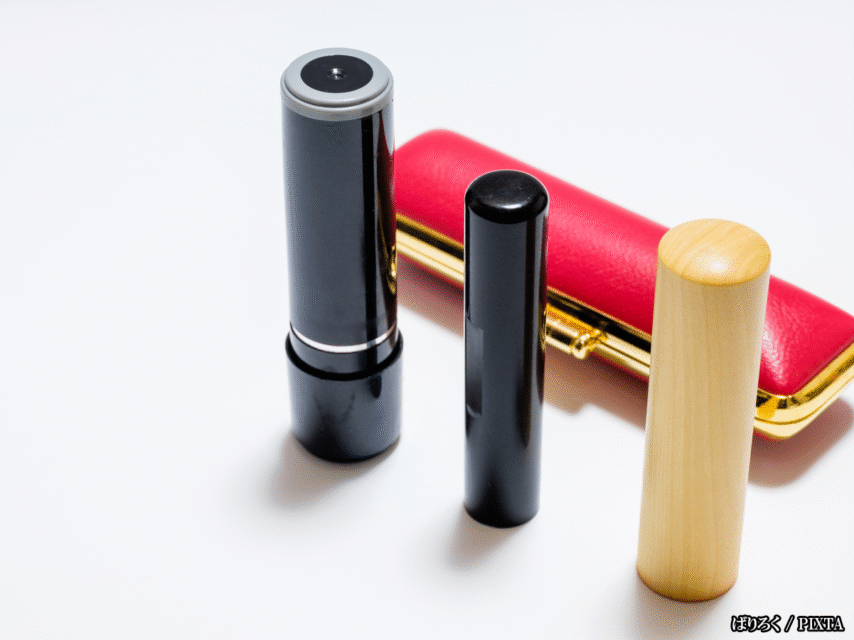

Choosing a ginkoin (size and material)

A ginkoin is a hanko used specifically for banking. It is not the same as your jitsuin (registered seal) and ideally should not be—using the same stamp for everything is a security risk. If one is compromised, the other remains clean.

Size

The standard size for a personal ginkoin is 13.5mm in diameter. This fits neatly within the designated stamp fields on bank forms and is the dimension most branch staff expect. Some people use 12mm stamps without issue, but 13.5mm is the safe, conventional choice for banking.

Material

This matters more than it seems. Banks occasionally reject impressions from soft rubber stamps because the impression is inconsistent—slightly different each time you press, which creates problems during verification. Harder materials produce cleaner, more reproducible impressions.

Recommended materials for a ginkoin:

- Resin (樹脂) — Durable, affordable, consistent impression. A solid choice for most people.

- Boxwood (柘植, tsuge) — Traditional, produces a clean impression, mid-range price.

- Titanium — Premium, extremely durable, consistent across years of use. Worth it if you plan to stay in Japan long-term.

Avoid cheap soft rubber or pre-inked disposable stamps for your ginkoin. They may be fine for parcel deliveries, but they introduce unnecessary uncertainty in a banking context where the impression is held on file.

Name format

Your ginkoin should carry your name in the same format accepted by your target bank—typically katakana for most foreign residents, though some banks accept romaji. If you have already confirmed with the bank which format they prefer, order accordingly. If you have not, katakana is the safer default.

HankoHub offers ginkoin specifically recommended for banking use, with guidance on size, material, and name rendering for foreign customers.

What to bring to the bank

Preparation here is the difference between a smooth thirty-minute visit and a return trip.

Standard documents required for foreign nationals opening a bank account in Japan:

- Residence card (在留カード) — Required at all major banks. Your name and address must be current.

- Passport — Not always required if your residence card is valid, but carry it anyway.

- Your ginkoin — Even at banks that accept signatures, arriving with a hanko demonstrates preparedness and may smooth the process.

- Initial deposit — Most banks require a small opening deposit. Even 1,000 yen is typically sufficient.

- Japanese phone number — Most banks require a contactable local number for account activation and notifications. If you do not yet have a Japanese SIM, sort this first.

- My Number card (マイナンバーカード) — Increasingly requested, particularly at larger banks. Not universally required but worth bringing.

A practical checklist before you go:

- Confirm the branch accepts foreign nationals (call ahead or check the bank’s English-language website)

- Ask specifically whether a seal or signature is required for foreign customers

- Verify that your residence card address is current and matches where you actually live

- Bring your hanko in an inkan case—it signals you are organised and taken seriously

- Arrive early in the day on a weekday; branch counters for new accounts can be slow in the afternoon

Some banks also ask you to complete paperwork in Japanese. If your Japanese is limited, bringing a translation app or a Japanese-speaking contact you can call for a quick question can prevent an otherwise avoidable delay.

Common mistakes

Using a mitome-in (everyday unregistered stamp) for your ginkoin registration

This technically works, but it creates a situation where the same stamp you use for casual office paperwork is also registered at your bank. If that stamp is lost, your bank account is exposed. Keep your banking hanko separate from your day-to-day stamp.

Ordering a ginkoin in a script your bank does not recognise

A kanji hanko is almost never appropriate for a foreign national’s ginkoin, because your registered name at the bank will be your romaji or katakana name from your residence card. Mismatches between the stamp and the account name create verification problems. Confirm the script before ordering.

Arriving without a phone number

This is the most common non-hanko reason foreign nationals are turned away mid-application. Japanese banks routinely require a local mobile number for SMS verification and contact purposes. A foreign number is usually not accepted.

Not checking branch-specific policy

Bank policy on seals, signatures, and foreign nationals varies by branch, not just by institution. What applies at a Shinjuku branch of a major bank may not apply at a rural branch of the same bank. One phone call before you go saves a wasted trip.

Bringing a hanko with an inconsistent impression

If you press your stamp on the application form and it looks slightly different from the next press, the bank may flag it. Practice pressing your hanko cleanly on scrap paper before you visit to ensure consistent, centred impressions.

FAQ

Do all Japanese banks require a hanko from foreigners? No. Digital banks like Rakuten Bank and PayPay Bank do not. Some branches of major banks accept signatures from foreign nationals. Traditional regional banks are most likely to require a seal. Check your specific target bank before assuming either way.

Can I use the same hanko for banking and official registration? You can, but it is not recommended. Your jitsuin carries legal weight and should be kept secure. Registering the same stamp at your bank means a lost or stolen hanko affects both your legal transactions and your bank account simultaneously.

What is the difference between a ginkoin and a jitsuin? A jitsuin is registered with your municipal office and carries legal weight for major transactions like property purchases. A ginkoin is registered with your bank for financial transactions. They are functionally separate, though the same physical stamp can technically serve both roles.

My name is very long. Will it fit on a hanko? Yes, with thoughtful design. A good hanko maker will adjust font size and layout to accommodate longer foreign names. For banking purposes, readability and impression consistency matter more than fitting every character at full size.

Can I open a bank account without any hanko at all? At digital banks, yes. At traditional banks, it depends on the branch and your nationality. Having a ginkoin available removes any uncertainty and gives you the most options.

How do I register my hanko with the bank? When you open the account, the bank will ask you to press your stamp into a designated field on the application form. This impression is stored on file. No separate registration process is required—it happens as part of account opening.

Next steps

Japanese banking as a foreigner involves more preparation than it should, but once your account is open and your ginkoin is on file, the system works reliably. The key step before your bank visit is having the right stamp—correct size, durable material, your name in the script your bank accepts, with a clean and consistent impression.

Shop bank-appropriate hanko at HankoHub, where ginkoin recommendations for foreign residents take the guesswork out of size, material, and name format. Getting this right once means you will not be dealing with mismatched impressions or rejected applications later.